A CEO’s Cost of Capital Advantage

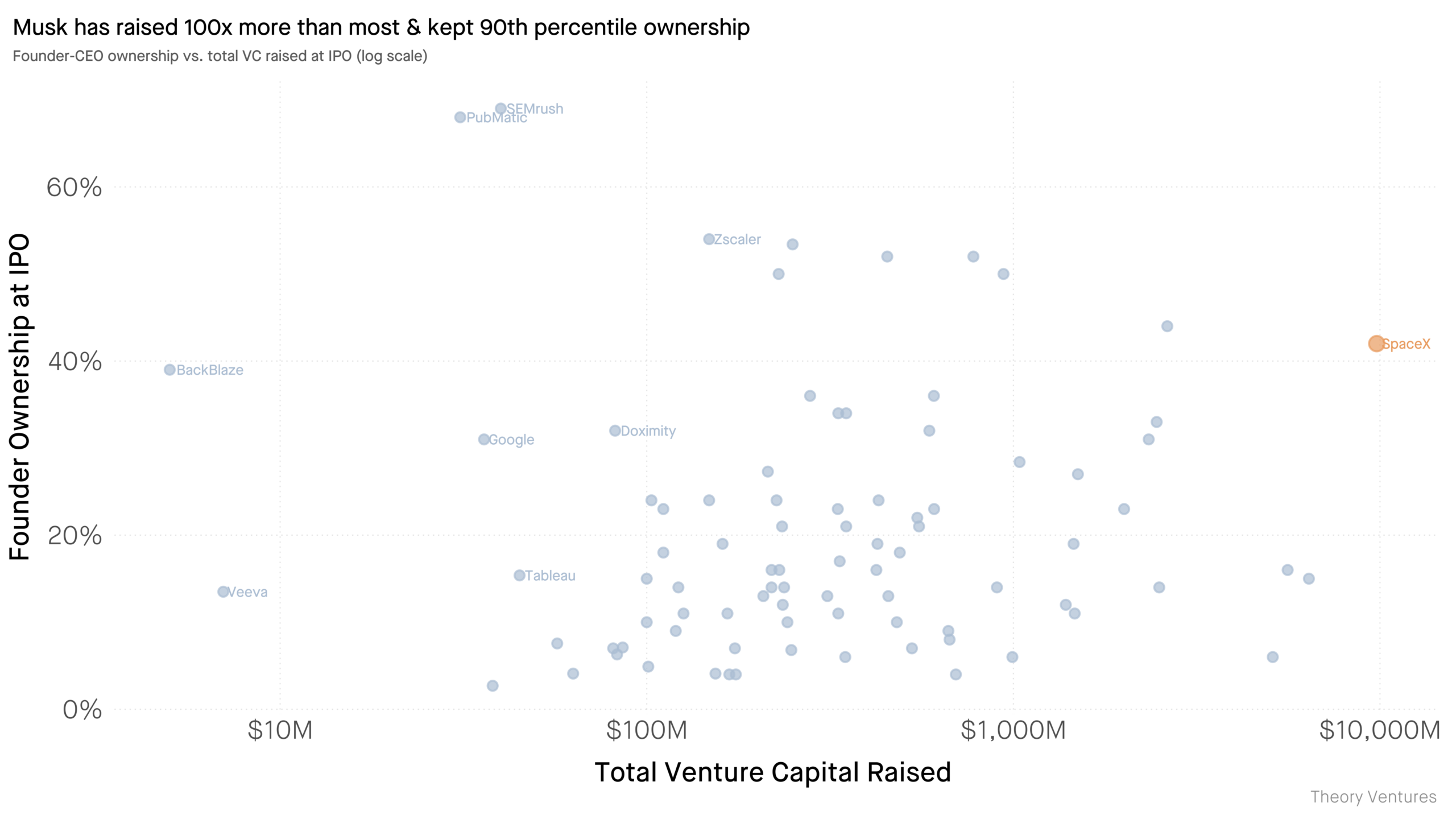

A founder’s personal cost of capital is often the invisible force that shapes how much they raise and how much they keep. This essay argues that while most analysis focuses on valuation or dilution, the real advantage comes from a founder’s ability to access cheaper capital from the start. Elon Musk’s trajectory from Zip2 to PayPal to Tesla to SpaceX is held up as the extreme example: he raised roughly 25x more than a typical founder yet retained ownership in the top decile. The core tension is that conventional startup advice treats capital as a commodity, but in practice some people pay a much lower price for it than others.

Early wins compound into a structural cost-of-capital advantage over time. The essay describes a flywheel: early fundraising success lowers the cost of the next raise, cheaper capital funds bigger bets, and bigger bets generate outsized returns. This pattern is visible in Tesla‘s retail ownership, which the source notes is 7x higher than the S&P 500 average, and in SpaceX allocating a large portion of its IPO to retail investors. The mechanism is not financial engineering but personal track record combined with public narrative that attracts capital from everywhere.

For a serious builder, the takeaway is that fundraising strategy should be treated as a personal capital efficiency problem, not just a valuation negotiation. Founders who can demonstrate early wins and build a credible narrative of compounding success will attract cheaper capital over time, which lets them retain more control while taking bigger swings. The essay suggests that the most important variable in venture financing may be the founder’s personal cost of capital, not the business plan or market size.